- Body

Enterprise budgets developed for rangeland-based ranching operations may include production activities for both crops (for example, hay and grain) and livestock (cattle, sheep, and goats). In each type of budget, there should be a description of the physical resources used in the production process as well as estimates of the typical returns and costs incurred.

Most budgets are presented in different sections for income, variable costs, and fixed costs. Income comes from the sale of the product being produced. If it is hay or grain produced on the ranch for use by the livestock enterprise, it is still evaluated as if it were sold in a market. Essentially, the livestock enterprise has to buy it from the hay or grain enterprise. Variable costs are those costs that change with the level of production. If you raise one more cow, what do you have to spend to raise it? Fixed costs are those things that you have to pay regardless of whether you produce any product at all.

Both variable and fixed costs can be cash or noncash costs. Cash costs are those that you are going to buy. Noncash costs are those things that are not paid for directly but include items such as operator labor, interest and depreciation on machinery, and interest on capital items such as land, machinery, breeding livestock, and buildings. Noncash costs are also referred to as opportunity costs since you could be using the funds or time tied up in the current enterprise in another investment.

Every ranch will have a different combination of variable and fixed items of production. Because of this, their variable and fixed costs will vary. Items and values shown in the sample enterprise budgets below should only be taken as guides. An individual rancher will need to find the enterprise budget closest to his operation and make the necessary adjustments.

Below are links to a few sample cattle enterprise budgets. Your local Cooperative Extension Service may have additional enterprise budgets for crops and livestock in your area.

The USDA Natural Resources Conservation Service provides information on state enterprise budgets

Oregon: 500 Head (Mountain Region)

Economic costs are used in the University of Idaho costs and returns estimates. All resources are valued based on market price or opportunity cost. This budget presents both the average costs and returns per cow for a 500-head cow-calf operation and the total costs and returns for the ranch. The forage source is federal, state and private range, and some feeding is necessary in the winter.

Livestock Investment - Livestock investment is 500 cows, 25 bulls, and 10 horses. Cows have a useful life of 5 years after they are placed in the breeding herd. The culling rate is 15 percent and the cow herd has a 2 percent death loss. The ranch buys two-year old bulls and replaces them every 4 years. The weaned calf crop is 88 percent of the number of cows wintered. Of the 95 weaned heifer calves selected from the calf crop for replacements, 10 are culled because of non-breeding or poor quality. This leaves a net replacement rate of 85 head each year.

Machinery and Equipment - The cow/calf enterprise uses two ¾-ton pickups (4x4), one 1-ton pickup (4x4), two 80 HP tractors (one with a loader), a feed wagon, a stock trailer, and a gooseneck trailer. This equipment complement is minimal, but considered adequate to make the ranch operation functional. Values on these investments are calculated at 50 percent of new replacement cost to reflect typically aged but functional ranch equipment. Haying equipment is not included in this budget as hay production is treated as a separate enterprise. Only equipment that is necessary for the cattle enterprise is included. Refer to EBB2-AH-03 for a summary of the costs and returns associated with hay production in southwestern Idaho. Hay and other feeds used as inputs in this cow/calf budget are valued at the market price received by growers (farmgate).

Buildings and Improvements - The ranch has 37 miles of 4-wire fence, one barn, a calving shed, one two acre corral with working alleys, a squeeze chute, a calf cradle and a normal complement of veterinary equipment. Water is supplied from natural sources. Buildings and improvements are valued at 80 percent of new replacement cost.

Oregon: 500 Head (Mountain Region)

This livestock enterprise budget estimates the typical costs and returns of producing calves in the mountain area of northeast Oregon (Wallowa, Union, and Baker counties, the eastern portion of Umatilla County, and the northern portion of Harney County). These areas are within the Blue Mountains Ecological Province and have a mixed conifer forest with many open meadows. It should be used as a guide to estimate actual costs and is not representative of any particular ranch.

The major assumptions used in developing this budget are discussed below describing the representative ranch.

Oregon Mountain 500 Head Livestock – The enterprise consists of 500 cows, 25 bulls, and 10 horses. A 95% conception rate is used, and 98% of the pregnant cows give birth. Cow death loss is 1%, bull death loss is 1%, and calf death loss is 5%. Mature cows are culled by 15% annually, and all replacement heifers are raised.

Calves are worked in April, including branding, vaccinating, and implanting. Cows are vaccinated in April and treated for external parasites. Cows and replacement heifers are vaccinated and pregnancy tested in the fall as the cattle are gathered. Cull cows, cull replacement heifers, and calves are sold November 1.

Livestock selling prices are a three-year average (2005-2008) of farmgate prices for the northeast region, including Baker, Crook, Grant, Morrow, Umatilla, Union, and Wallowa counties. Livestock weights are assumed typical for the mountain area.

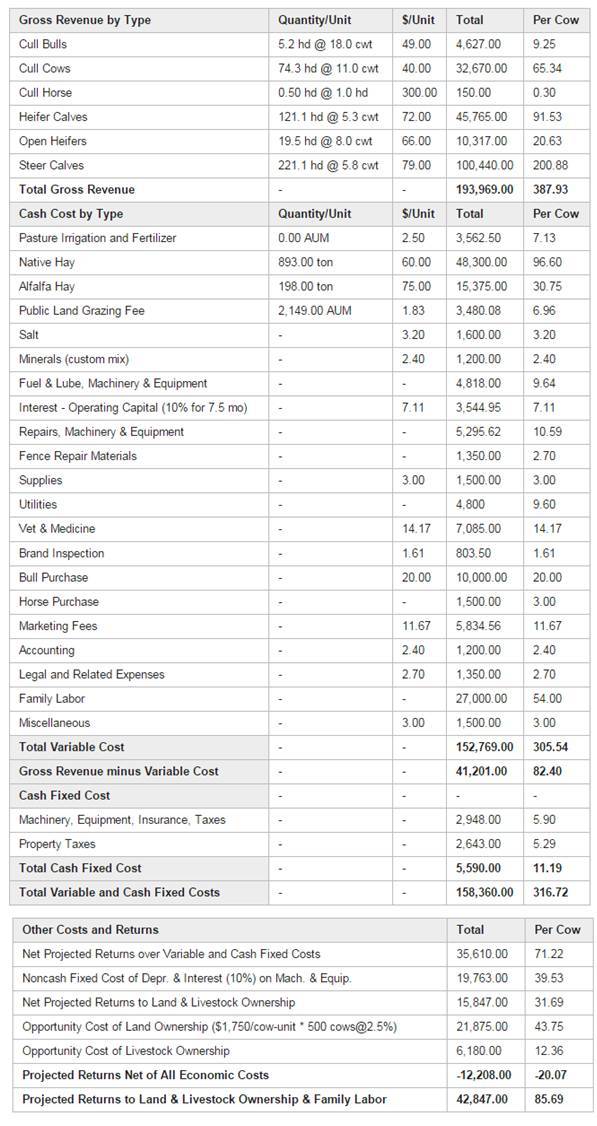

Table 1. Oregon Cow/Calf Costs and Returns, Mountain Region, 500-Cow Herd

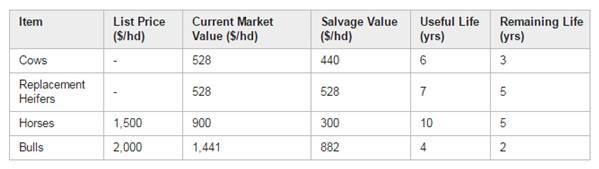

Table 2. Livestock Cost Assumptions

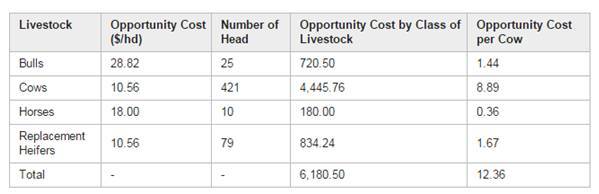

Table 3. Livestock Opportunity Cost Calculations

Oregon Mountain 500 Head Feed - Feed is supplied in the form of native and feeder-quality alfalfa hay, public range, and pasture. Cattle are fed hay for four and a half months, forest service range is used for three and a half months, privately owned spring range is grazed for one and a half months, and stringer meadows are utilized for the remaining two and a half months. A $2.50 per AUM charge covers fertilizer and irrigation expenses for the private pasture.

Salt and minerals are fed at the rate of 48 pounds per cow annually, and approximately one-third is assumed to be consumed by wildlife.Oregon Mountain 500 Head Labor - Labor provided by two families is included as a variable cost of $27,000 per year, assuming eight months are dedicated to the cow/calf operation and four months to hay production.

Oregon Mountain 500 Head Labor Capital - Opportunity costs of operating capital are charged at a rate of 10 percent for the duration of the grazing season and 2.5 percent per year for the current market value of the ranch unit, including land and livestock.

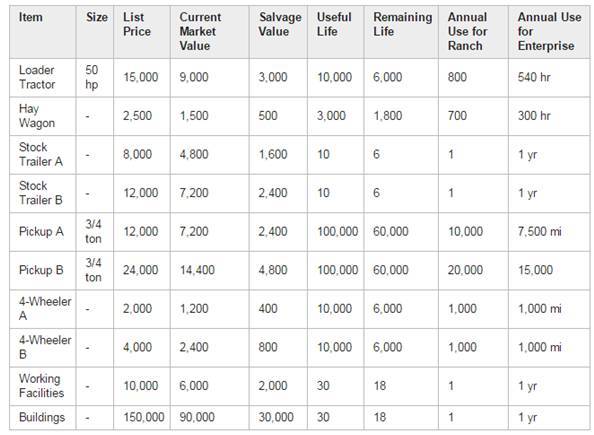

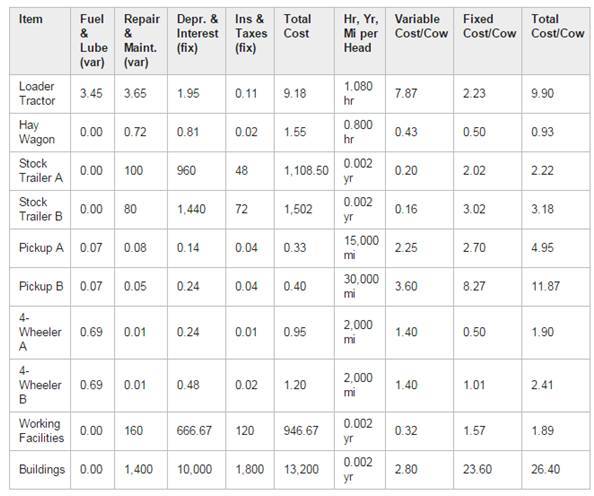

Oregon Mountain 500 Head Equipment - A loader tractor and hay wagon are used to feed hay. A 3/4-ton pickup is used to pull a stock trailer, for general travel, and for general ranch work. Corrals are used in the spring and fall to work cattle. Two four-wheel ATVs are used for general ranch work.

Machinery and equipment values are based on spring 1996 replacement costs, assuming the assets are half depreciated. Table 4 summarizes the values assumed for machinery, equipment, and buildings as well the hours, miles, or years associated with their use. "Working Facilities" include a squeeze chute, corrals, and scales.

Machinery and equipment costs are shown in these tables for variable and fixed cost components.

Table 4. Machinery Cost Assumptions

Table 5. Machinery and Equipment Cost Calculations

Oregon Mountain 500 Head Resources - The commercial value of land and improvements of a whole ranch unit ranges from $1,000 to $2,500 per cow unit (animal unit) depending upon productivities and extent of federal land dependency. This budget assumes that the ranch as a whole is valued at $1,750 per cow unit. The operator owns 4,100 acres of spring range and 1,480 acres of improved spring range, providing 410 and 1,150 AUMs, respectively, over one and a half months. In addition, 725 acres of stringer meadow is owned and supplies 1,425 AUMs over two and a half months. Property taxes total $2,643. Actual property taxes will vary with assessed value.

Oregon Mountain 500 Head Other Costs - In the enterprise budget, implants, pour-on, vaccines, pregnancy testing, fly tags, and dewormer are included under the line item "Vet & Medicine." Brand inspection is $1.75 per animal sold, plus a $10 per trip charge with three trips assumed. Materials for fence repairs cost $1,350. "Supplies" include saddle, tack, and branding equipment. "Marketing Fees" are a flat 3% of the gross value of the livestock that are sold to cover marketing costs via satellite or through the auction yard, etc. "Utilities" include electricity, telephone, and others. "Legal and related expenses" cover costs associated with litigation regarding policy issues and other legal expenses. All items not included in the other budget line items, such as association dues, are accounted for under "Miscellaneous."