Written by John Tanaka, University of Wyoming

A ranch is a business and managing a ranching enterprise based on a resource as varied as rangelands poses unique challenges. The financial success of a ranching enterprise depends on many variables and is affected by many different factors and their interactions.

- Ranch Planning - Planning is a critical activity for a ranch to be economically, socially, and ecologically successful. There are many resources available to ranchers to assist them in planning. Most are similar and the important thing is to select one and do it. Planning generally involves setting goals and objectives, inventorying all resources, developing resource use activity plans, implementing, and monitoring followed by adjustments.

- Livestock Demographics in Rangeland States - Livestock numbers for beef cattle, sheep, and goats are available from the U.S. Census of Agriculture.

- Ranch Budgets - Budgets for ranches are used as management tools to help ranchers make decisions on the business side of their operations. There are four basic types of budgets that can be used: whole ranch, partial, cash flow, and enterprise. Each of these budget types are developed to estimate how the operation will look in the future as opposed to records that describe what happened in the past.

- Production Economics - Livestock production on rangelands is generally done for the operator to make some level of profit. While we know that profit maximization is not the reason most people choose to go into ranching, for most, they do need to at least break even to stay in business. This section will look at traditional methods to analyze the economics of livestock production.

- Financial Record Keeping - Financial records for ranches are an important management tool. Book keepers will normally generate these sorts of reports for a ranch business. Our focus here is on how to interpret the different sorts of financial records for making management decisions. The basic financial records are the balance sheet, income statement (profit-and-loss), and cash flow. A brief description of each one is provided.

- Drought and Economics - Drought on rangelands is a normal occurrence. Drought causes periods of reduced forage and water availability to grazing animals. This section will describe the economic impacts on ranching operations.

- Agricultural Subsidies - Ranchers do not generally receive direct subsidies for their operations. The Natural Resources Conservation Service through their many conservation programs can provide direct assistance for specific practices. In addition, other U.S. Farm Bill programs can affect production and prices of inputs (e.g., grains) used by ranches.

- Forage Lease Rates - Private, state, or federal forage may be leased by a ranch. Each source of forage may be priced differently based on the different levels of services provided and forage quantity and quality.

- Alternative Enterprises - With the increasing recognition of ecosystem goods and services from rangelands, ranchers may consider their ability to increase their income through producing and marketing those goods and services. There are examples such as selling hunting leases or improving lands for water production that have led to increased income for ranchers. Ranchers need to carefully evaluate their options and determine how they fit into their goals, objectives, and management.

- Grazing Management Economics - Defining the economics of grazing management is a difficult task. There is no one right answer. This section will look at how the economics could be evaluated from a management perspective. When grazing management changes are contemplated on a ranch, there are several factors that need to be examined that will each affect the economics of the practice. These factors include: changes in animal productivity, changes in how pastures are used, changes in feed sources, changes in animal husbandry, changes in infrastructure, and changes in management.

- Economics of Predation on Rangeland Operations - Predation of livestock has both direct and indirect losses to the ranch. The direct losses are due to losing animals to predators (e.g., coyotes, bears, wolves, eagles). Indirect losses may include time spent determining the predator, predator control, and changing management to reduce predation.

- Economics of Poisonous Plants - Poisonous plants on rangelands can be either native or introduced species. Different poisonous plants can affect different grazing animals differently. Depending on the severity of reaction (mild illness, abortion, reduced production, death) and potential treatments, the plant will have different levels of economic impact on the ranch. In addition, at times different management of the animals or plant control methods may be required that increases the cost of production.

Ranch Planning

Written by John Tanaka, University of Wyoming

Western ranches have been owned and operated for a variety of reasons. These include way of life, profit as a business, an investment, or an occupation. For most, these are not exclusive goals, but the relative importance dictates how decisions may be made. A ranch business plan provides a framework for setting goals, collecting information, analyzing that information, and serving as a guide for implementing what was decided upon.

As one example, the Wyoming Business Council has developed a workbook titled "Sustaining Western Rural Landscapes, Lifestyles, and Livelihoods" to guide the development of a ranch plan. The workbook is located on the Sustainable Rangelands Roundtable website for Ranch Sustainability Assessment. The basic process is for the ranch family to identify personal values and goals; develop a needs assessment and resource inventory; conduct a strength, weakness, opportunity, and threat (SWOT) analysis; evaluate feasibility of options; determine if personal goals can be met; implement needed changes; and reevaluate.

Ranch Budget

Budgets for ranches are used as management tools to help ranchers make decisions on the business side of their operations. Four basic types of budgets can be used: whole ranch, partial, cash flow, and enterprise. Each of these budget types is developed to estimate how the operation will look in the future as opposed to records that describe what happened in the past.

Whole-Ranch Budgeting - Whole-ranch budgets are used primarily to compare alternative ranch organizations under different production patterns, to evaluate the whole-ranch profitability potential, and to provide projections to potential lenders, consultants, and others who need to understand the whole operation.

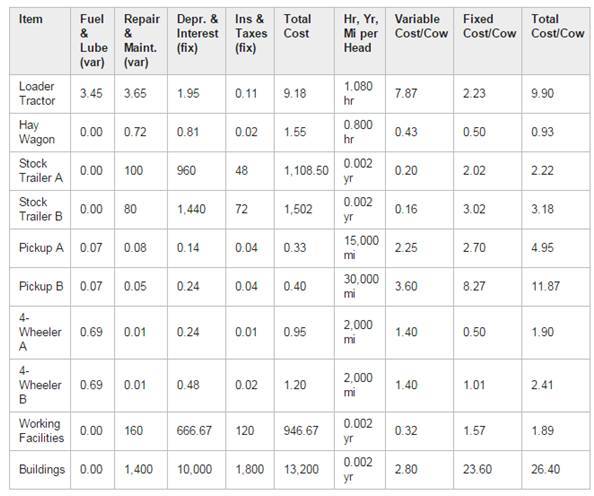

Partial Budgeting - Partial budgets are used primarily to examine minor changes in the whole-ranch plan. It only includes those items and values of things that are likely to change and are not expected to be so large as to impact the whole ranch operation. Partial budgets are appropriate to economically evaluate small management changes on the ranch. The process is to estimate the changes in both costs and benefits as shown in the table below and then to simply add the values. If the costs or benefits occur over a number of years, the future values should be discounted back to present value before summing. If costs increase, they are shown as being more negative, and if they decrease, they will be a more positive value.

Cash Flow Budgeting - Cash flow budgets help you plan the timing of income and expenses in a specific time period. They are typically set up on a monthly basis and are of interest to lenders to ensure you will have the cash to repay a loan.

Enterprise Budgeting - Enterprise budgets list all of the income and expenses associated with producing one enterprise in a particular manner. An enterprise is defined as any activity that results in a product that is either used on the farm in other enterprises or sold in the marketplace. Enterprise budgets are used to estimate income and expenses as well as listing physical resources needed for production. Enterprise budgets are detailed and time consuming to construct. Most Cooperative Extension offices have access to sample enterprise budgets for most livestock and crop activities. These examples use typical production practices and prices and do not necessarily represent averages. Ranchers can use these typical enterprise budgets as starting points and use their own estimated values.

Financial Records

Written by John Tanaka, University of Wyoming

Financial records for ranches are an important management tool. Bookkeepers will normally generate these sorts of reports for a ranch business. Our focus here is on how to interpret the different sorts of financial records for making management decisions. The basic financial records are the balance sheet, income statement (profit-and-loss), and cash flow. A brief description of each one is provided below.

Similar statements are shown in the budgeting section. The difference is that these records are an evaluation of the past, whereas the budgets are to help forecast the future.

Balance Sheet - A balance sheet shows a snapshot in time of the financial state of a business. It will normally list the short, medium, and long term assets compared to the short, medium, and long term liabilities of the company. Subtracting the total of liabilities from the total of assets provides the owner's equity or net worth.

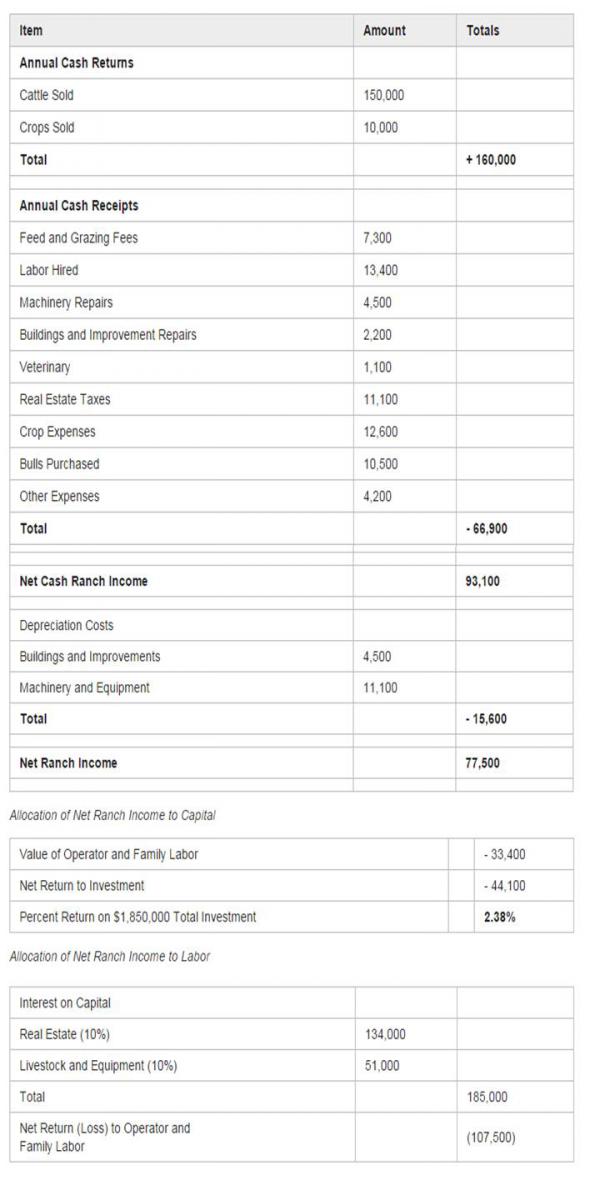

Ranch Income Statement - The income statement shows the income and expenses incurred over a given time period, usually a year. There is a standard income statement and a modified income statement that may be useful in certain situations.

The standard income statement shows the annual returns from sales of ranch products and the cash and non-cash expenses used to produce it. The net ranch income is then allocated to "capital" or to "labor." Allocating it to capital allows the rancher to calculate a return on investment. Allocating it to labor allows the rancher to calculate what was earned for the year's work.

The modified income statement helps answer two questions that the standard one makes difficult to answer. Will the ranch produce enough income to live on after all operating expenses are paid? How much net income is made to compensate owned capital (owner's equity)? These two questions will provide insight into why someone would invest in a ranch and how a rancher can stay in business when receiving a relatively low rate of return on a large investment in land and improvements.

Example:

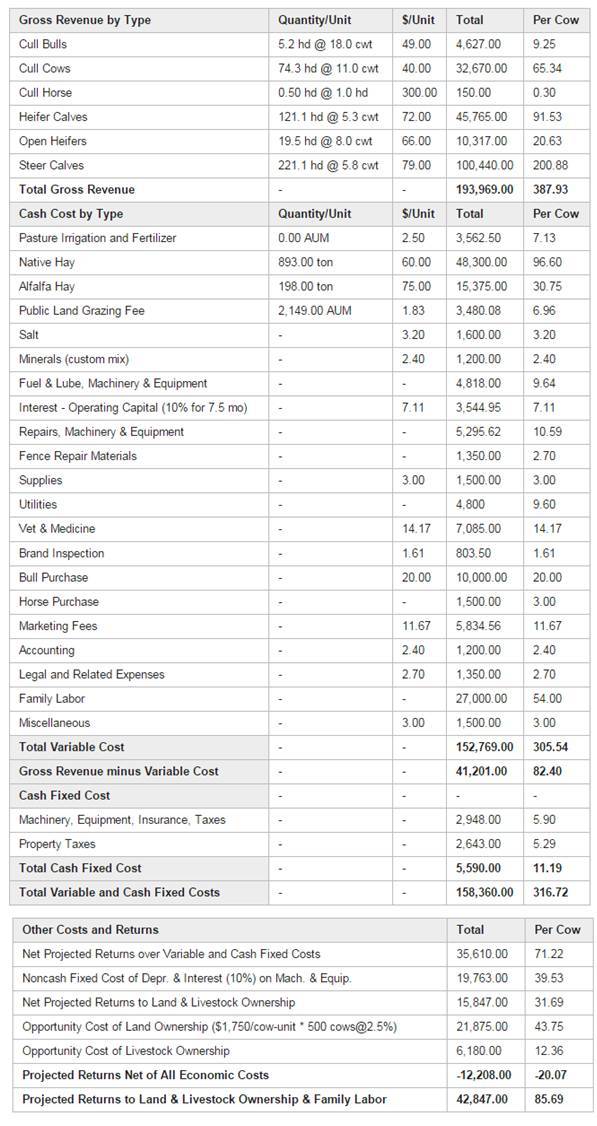

The standard income statement is shown in Table 1 for a hypothetical 300-cow ranch. The standard income statement seeks to allocate net income to either capital or labor.

Table 1. Standard income statement for a hypothetical 300-cow ranch, 2008.

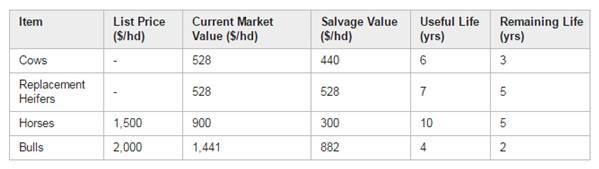

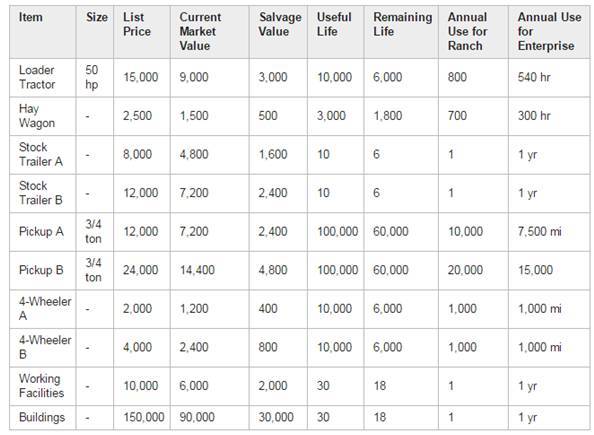

To allocate net income to capital, a charge for operator and family labor must be deducted and the residual divided by the total investment in the ranch. Note that total investment is the value of land, buildings, improvements, machinery, and livestock without regard to who actually owns it, the operator or the lender.

To allocate net income to labor, a charge for the interest on capital must be made. That amount is subtracted from the net ranch income to show the operator what their time was worth on the ranch. The premise is that all capital should earn a fair return whether it is owned or not.

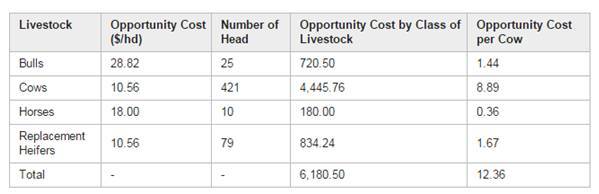

Both the interest on owned capital and operator and family labor are opportunity costs. They do not have to be paid as long as there is enough net income available on which the family can live.

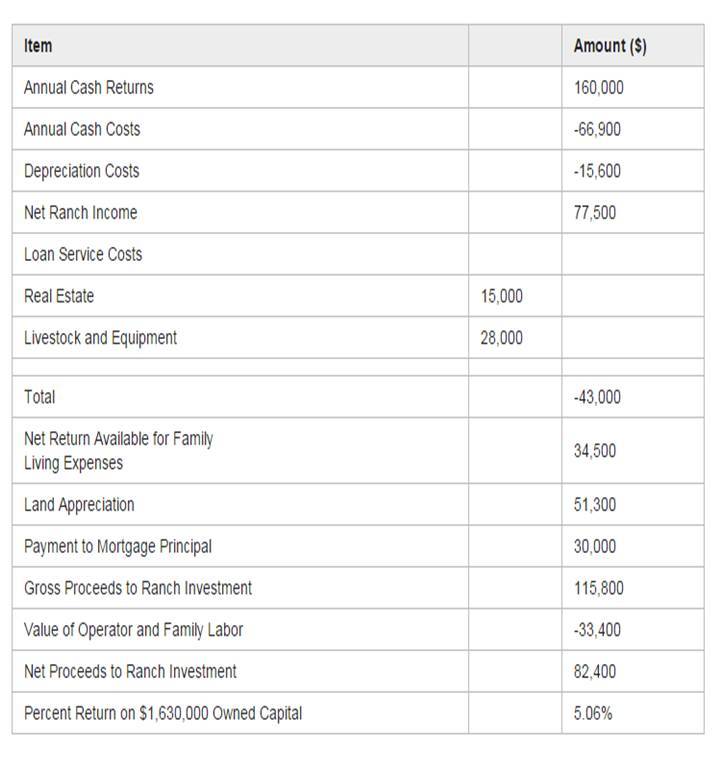

Modified Income Statement - The modified income statement starts with the same basic information as the standard version in calculating net ranch income. It differs from that point on in trying to answer these questions:

● "Will the ranch produce enough net income for the family to live on?"

● "How much net ranch income is available to compensate investment of owned capital?"

The first question is addressed by subtracting the loan service cost payments that must be made. The amount available for family living expenses is an accurate amount of what the family has in the way of cash from this operation. It can be combined with the perquisites of ranch living that are often covered as business expenses such as utilities, automobiles, housing, and home-grown food.

Adding in a value for land appreciation and the amount of mortgage principal repaid during the year provides an estimate of the long-term ranch income. Of course, this amount is not realized as income unless the ranch is sold or loans taken out, but it is an indicator of the potential from the ranch.

By putting a charge for operator and family labor against the gross proceeds, we get an estimate of net proceeds that is attributable to the owned equity of the ranch. The result shows a much higher rate of return and helps explain why someone would invest in a ranch.

The modified ranch income statement has at least three benefits over the standard income statement:

1. It is more realistic. Real estate appreciation is treated as a real source of income. Investors often buy real estate with the hope that it will appreciate faster than the rate of inflation and thus treat it as a real return when making their decisions.

2. It is much simpler. It is not necessary to use hypothetical rates of return on capital to allocate net income to labor. Ranchers can look at the actual generated rates of return and evaluate whether that meets their goals.

3. It is easier to interpret. The net return is actually what the ranch family has to live on, and the rate of return is what their investment is earning.

Table 2. Modified income statement for a hypothetical 300-cow ranch, 2008.

Cash Flow Statement - Cash flow statements are used to show how the income coming into the business is being spent in each time period. These can be set up for any length of time period and are used in a budgeting sense to ensure that there is always enough cash income available in that period to cover the cash expenses.

Workman, John P. 1981. Analyzing ranch income statements - a modified approach. Rangelands 3(4):146-148.

Forage Lease Rates

Written by John Tanaka, University of Wyoming

Forage for domestic livestock is leased on both public and private lands. Public land forage lease rates are administratively set using the formula defined in the Public Rangelands Improvement Act.

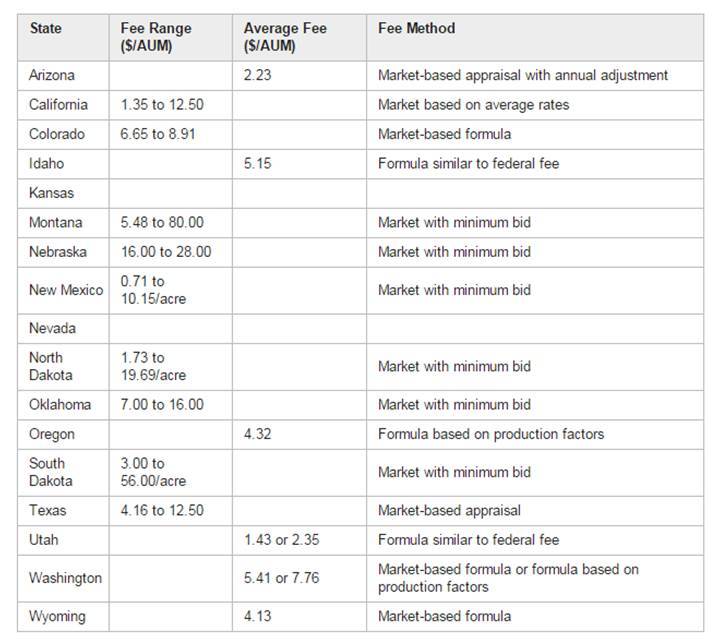

State-owned lands are leased with each state using its own methods for setting the lease rate. Some states follow the federal formula adjusted for their own conditions, some modify the formula, some base it on the private land lease rate in their state, and some use a cost-share formula.

States were generally allocated two sections of land out of each 36 sections (a township) for the purpose of generating income to support schools. These school sections have been treated differently by each state but are generally set aside to maximize income to the school trust. In states that have retained ownership of school sections suitable for grazing, each state has developed a somewhat different method of setting the grazing fee. The Government Accountability Office (GAO) conducted a study in 2005 that reported the different grazing fees in the western states. These fee ranges or average fees are shown below.

State Lands Grazing Fees (2004)

Private land lease rates are determined through private negotiations between the landowner and the lessee. The USDA National Agricultural Statistics Service collects data for each of the 17 western states (Arizona, California, Colorado, Idaho, Kansas, Montana, North Dakota, Nebraska, New Mexico, Nevada, Oklahoma, Oregon, South Dakota, Texas, Utah, Washington, and Wyoming). This information is published in the January edition of the Agricultural Prices publication each year.

Source: Government Accountability Office. 2005. Livestock Grazing - Federal Expenditures and Receipts Vary, Depending on the Agency and the Purpose of the Fee Charged. GAO-05-869. 110 p.

Grazing Management Economics

Written by John Tanaka, University of Wyoming

Defining the economics of grazing management is a difficult task. There is no one right answer. This section will look at how the economics could be evaluated from a management perspective.

When grazing management changes are contemplated on a ranch, several factors need to be examined which will each affect the economics of the practice. These factors include changes in animal productivity, how pastures are used, feed sources, animal husbandry, infrastructure, and management.

Changes in Animal Productivity - As grazing management is changed, the livestock will be in different pastures and under different kinds of stress from their previous system. More frequent moves of livestock can have an adverse effect on their weight gains, their reproductive success, and the quality of the product that comes from them. Each of these can affect the total value of the product.

Pasture Management - As pastures are used at different times of the year and different intensities, there can be an effect on both productivity and quality. In addition, more frequent moves can increase labor costs. There may also be a need to change fertilization or irrigation on improved pastures, hay meadow use, and seeding on pastures or rangelands.

Changes in Feed Sources - As grazing management changes, there can be an impact on other feed sources. Because the livestock have to be fed every day, a change in one area requires a change in another. Potential economic impacts include different hay feeding seasons, different uses of leased or permitted lands, different uses of feed supplements, and concurrent changes in labor costs.

Changes in Animal Husbandry - This topic is related to animal productivity. Additional change in how livestock are raised can affect breeding and calving seasons, medical care, weaning dates, and general animal care that will affect both input and labor costs.

Changes in Infrastructure - As grazing management is changed, there may be a need to install, maintain, or remove different parts of the ranch infrastructure. Fences and water developments would be the most common infrastructure investments that would be considered. Improvements in seeded pastures or rangelands, irrigation systems, corrals, barns, and other such infrastructure should be considered.

Changes in Management Last, but probably most important, changes in management will be a critical consideration. As grazing management is changed on a ranch, the manager needs to ensure that all the pieces fit together and work as expected. The manager is likely to have to invest more time in implementing the changes, monitoring how things are working, and making adjustments.